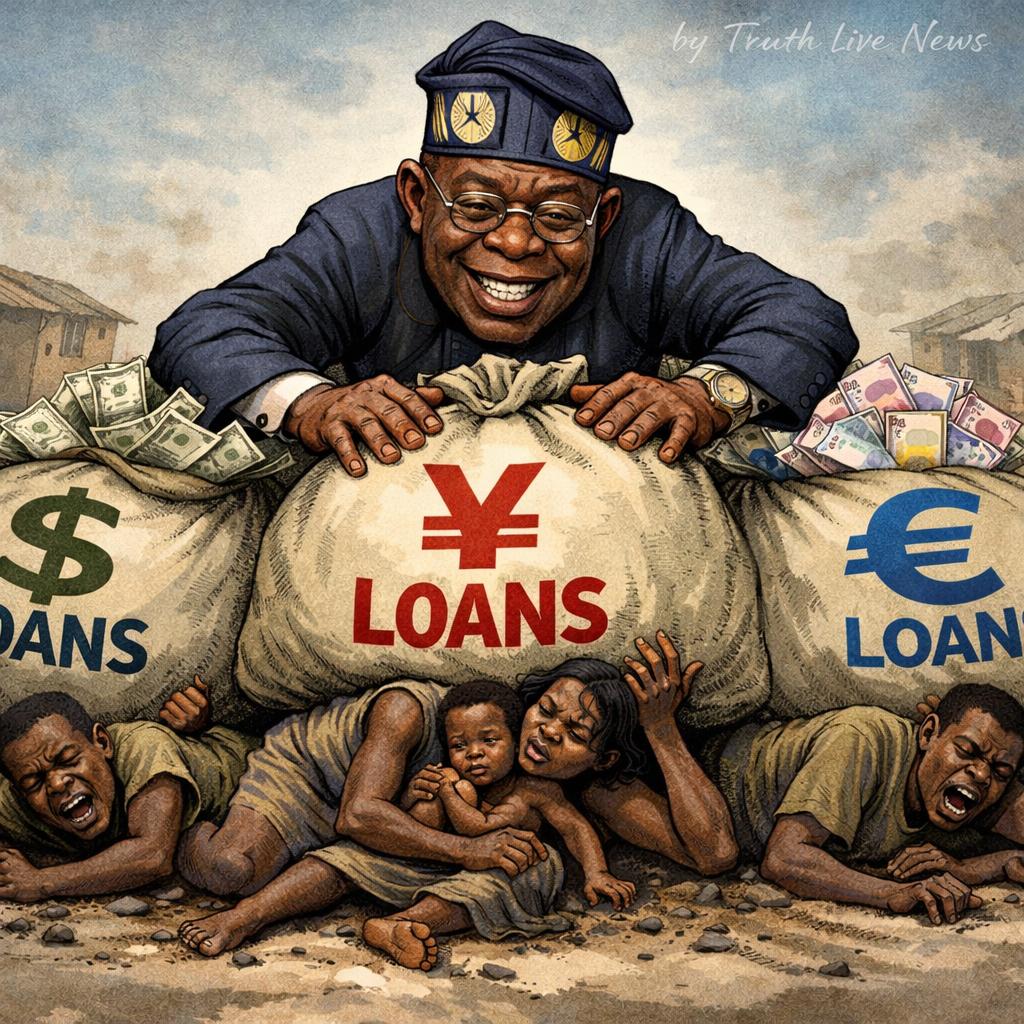

Nigeria today stands on the edge of a deep fiscal precipice, one that has been recklessly engineered under the leadership of President Bola Ahmed Tinubu. Since assuming office in May 2023, his administration has presided over a staggering escalation of the nation’s public debt, pushing it from about ₦87 trillion to over ₦153 trillion within a short span. According to figures from the Debt Management Office and corroborated by Reuters reports, this near ₦66 trillion surge is not just a statistic, it is a loud alarm bell of economic mismanagement, policy recklessness, and a troubling absence of tangible development to justify such borrowing.

What makes this debt accumulation particularly alarming is not merely its size, but its speed and the conditions under which it has grown. In less than three years, Nigeria has witnessed one of the fastest expansions of public debt in its history. Yet, there are no commensurate infrastructural breakthroughs, no visible nationwide economic transformation, and no meaningful upliftment of the average citizen’s living standard. Instead, Nigerians are confronted daily with worsening inflation, collapsing purchasing power, and deepening poverty.

The administration may attempt to deflect by attributing part of the debt surge to exchange rate fluctuations and the securitisation of so-called Ways and Means advances. However, such explanations only scratch the surface. The reality remains that Tinubu’s economic decisions, particularly the abrupt devaluation of the naira, have significantly inflated Nigeria’s external debt in local currency terms. This is not an accidental outcome, but a direct consequence of policy choices that lacked adequate safeguards for economic stability.

Even more concerning is the scale of new borrowing being pursued under this government. Reports indicate that Tinubu sought and obtained legislative approval for over $21.5 billion in fresh external loans, alongside additional euro, yen, and domestic dollar denominated borrowings. This aggressive appetite for loans, at a time when debt servicing already consumes a large chunk of national revenue, raises serious questions about fiscal responsibility and long term sustainability.

One would expect that such massive borrowing would translate into visible and measurable development outcomes. Sadly, that expectation has not been met. Across Nigeria, infrastructure remains largely stagnant, power supply continues to falter, and critical sectors such as education and healthcare remain grossly underfunded. The ordinary Nigerian sees no reflection of these trillions in their daily realities, only hardship.

It is important to understand that borrowing in itself is not inherently problematic. Nations borrow to invest, to build, and to stimulate growth. However, borrowing without accountability, without strategic deployment, and without visible returns is nothing short of economic sabotage. Under Tinubu, Nigeria appears to have crossed that dangerous line, where debt is accumulated not as an instrument of growth, but as a burden passed onto future generations.

The argument that some of the debt increase stems from legacy issues or previously accumulated obligations does not absolve the current administration of responsibility. Leadership is defined by the ability to manage inherited challenges effectively, not to compound them. Instead of stabilising the economy, Tinubu’s policies have exacerbated existing vulnerabilities, deepening Nigeria’s fiscal crisis.

Furthermore, the sharp rise in domestic debt reflects an over reliance on internal borrowing, crowding out private sector access to credit and stifling economic expansion. When government dominates the borrowing space, businesses struggle to access funds, investment slows, and job creation suffers. This is the silent but devastating impact of fiscal mismanagement.

The consequences of this debt trajectory are already evident. Nigeria now spends an alarming proportion of its revenue on debt servicing, leaving little for capital projects and social services. This creates a vicious cycle where more borrowing is required to fund basic governance, further worsening the debt profile. It is a cycle that, if left unchecked, could push the nation into a full blown fiscal crisis.

Tinubu’s defenders may argue that reforms take time, that economic restructuring is a gradual process. But governance is not judged by intentions, it is judged by outcomes. And the outcomes so far are deeply troubling. Rising debt, rising inflation, and rising hardship cannot be the foundation upon which any credible reform agenda is built.

There is also a growing trust deficit between the government and the governed. Nigerians are increasingly questioning where these borrowed funds are going. Transparency has been limited, accountability mechanisms appear weak, and public confidence continues to erode. In any democratic society, such opacity is dangerous and unsustainable.

History will not be kind to an administration that borrowed so heavily without delivering meaningful progress. The numbers are already written in stark clarity, ₦66 trillion added to the nation’s debt burden with little to show in terms of transformative impact. This is not merely an economic issue, it is a moral one.

Nigeria deserves better. It deserves leadership that borrows with purpose, spends with discipline, and delivers with integrity. Until that standard is met, the current trajectory remains a painful reminder of missed opportunities and a future mortgaged by reckless decisions.

Deacon Amb. Darlington Okpebholo Ray, Journalist and Publisher of Truth Live News International, writes from Greenwich, London, United Kingdom.